Hey Stress-Free Budgeteers! We have a special topic to explore today – the deeply-rooted psychology of money and how it can affect your decisions in the short-term, and ultimately, your mindset in the long run.

It’s a deep topic for most of us since money is a crucial aspect that touches on our lives on many levels.

However, despite many resources floating around on our website, many people still ask me how to get their stressful money management in order – which is why I created this blog post to identify and understand what’s keeping your relationship with money at arm’s length.

This article will take a closer look at various emotional aspects and how these emotions can affect your mindset.

The psychology of money is the study of our emotional relationship with– you guessed it, money.

Being mindful of your money isn’t about how great you are at maths, It touches up on our beliefs, behaviours, and attitudes– and how these behaviours can affect our thinking.

Does It Matter? Absolutely!

We all have certain behaviours and patterns that play out every day, especially in stressful situations where we have to think of decisions on the spot.

And money is a massive trigger to that problem.

Understanding these triggers, especially when around money, is a superpower that allows us to break free of the emotional triggers and rise above them.

Most of the time, when people make decisions, they come from a very logical and practical standpoint where emotions are sidelined. This is particularly true when mulling over a particularly significant decision like an investment-related opportunity.

But sometimes, we slip up and let our financial decisions be guided by emotions rather than logic and reasoning. When emotions override our reasoning, it can lead to making some unfavourable choices.

But don’t worry, allowing our emotions to affect our money-related choices happens to the best of us– it happens to us on a regular basis, don’t worry!

So, what are these emotions?

First up, fear – this emotion mainly comes to us in the form of not having enough money. When under the grip of fear, we are under the spell of making impulsive choices that we’ll learn to regret later.

Fear comes in many forms, but all the more deadly. Here’s one of the most common examples that I have noticed in many of my clientele:

Fear can come in the form of shortage. People who grew up with very little can develop a deep-seated fear of not having enough money.

As a result, they may develop a mindset of living an extremely frugal lifestyle, where they save every dollar they can get their hands on at the expense of their quality of living.

While this lifestyle is a choice people are free to make, I do not recommend going to this extent since this mindset can lead to hidden consequences.

For example, someone close to you might avoid going to the doctor since they worry about the necessary medical expenses, prescribed medications and the cost they might bring once they find out they have a condition.

Sounds like someone you know, right?

Greed is another heavy-hitter that can have an adverse effect on our decisions and more often than not, greed can creep up on us in several ways.

This emotion is probably the deadliest one since it can lead you to prioritise short-term victories over long-term stability, security, and happiness.

How? Here’s a great example.

Imagine that someone you know poured their life savings into a volatile, but rewarding investment with the hope of making serious cash fast (e.g. the crypto market) even if they are fully aware that they might also incur significant losses.

If this scenario hits close to home. That’s greed in the sense that they want to make significant gains.

How? They prioritize getting rich fast over prudent money management.

Let’s get more personal with another example. In a family setting, greed can come in the form of reluctantly sharing financial responsibilities with your partner.

Sure, you’re dividing the burden with your partner, but does it really sit right with you?

For shame, this emotion comes when we either let ourselves or our family members down financially– this can happen due to debt, job loss, or foreclosure.

A little voice in the back of our head will then tell us to go to great lengths to hide these difficulties and pretend everything is fine and will be fine. It’s an all too familiar feeling that we hate the most.

For example, some married couples avoid discussing each other’s financial situation openly because they are ashamed of getting judged as less successful than their partner.

This emotion can lead to feelings of “being not enough” for the lesser income-earning partner, which can minimize communication with their partner, which then results in poor financial planning and misunderstandings in the future.

Additionally, an adult who was down on their luck and had to resort to staying with their parents may also experience shame for not being financially independent.

This shame can force you to hide your current situation from your close friends and colleagues who are more self-sufficient.

Happiness is a double-edged sword that can either positively or negatively affect our money-making decisions, but more often than not, happiness can lead to impulsive choices.

How? When we overcome a difficult situation, we tend to become excited and ignore our reasoning. We then indulge ourselves in rewards and next thing you know, you have overspent more than you should.

However, here’s the thing; if these emotions are currently present in yourself and you have identified that these emotions are taking the wheel from you, congratulations!

This is just the first step in taking more control of your mindset.

So don’t feel bad, it’s a completely ordinary reaction people have! But how do we make use of these feelings?

We’ll get to that later. First, we’ll have to talk about brain shortcuts and how they have a hand together with your emotions in most of your decisions.

While we can easily recognise emotions, even in the heat of the moment, brain shortcuts are deadly because your own mind is actively working against you.

Brain shortcuts are “optical illusions” we unconsciously place in our minds that affect how we perceive our decisions. These shortcuts are lethal in the sense that they can streamline complex information into simplified ones.

These simplified decisions can often lead to gaps in our judgment, and when combined with the emotions mentioned above, can make money-related decisions harder than they should be.

Defined as heavily relying on the first piece of information we receive– regardless of accuracy– is the most widespread brain shortcut out of the four listed here.

An everyday example can be found in the context of shopping, especially during sales or discount events. Here's how it can typically play out:

Imagine you're shopping for a new smartphone. You walk into an electronics store, and the first smartphone you see has a price tag of $999. This initial price, often referred to as the "anchor," immediately grabs your attention.

As you continue browsing, you come across another smartphone with similar features, but its price is listed as $799. Now, your perception of the $799 price is heavily influenced by the $999 you saw earlier– a bargain!

Cue the purchase, now you have two smartphones. Now, what…

That’s what makes this shortcut so dangerous. It can affect most significant money-management decisions like buying a car or investment opportunities to even everyday choices like eating out or grocery shopping.

Once this shortcut takes hold of your mind, the can persist and continue to influence decisions, even when you’re aware of how irrational it’s making you.

Understanding this brain shortcut can help us avoid the pitfalls of deceptive pricing strategies, leading to savings from impulsive buying.

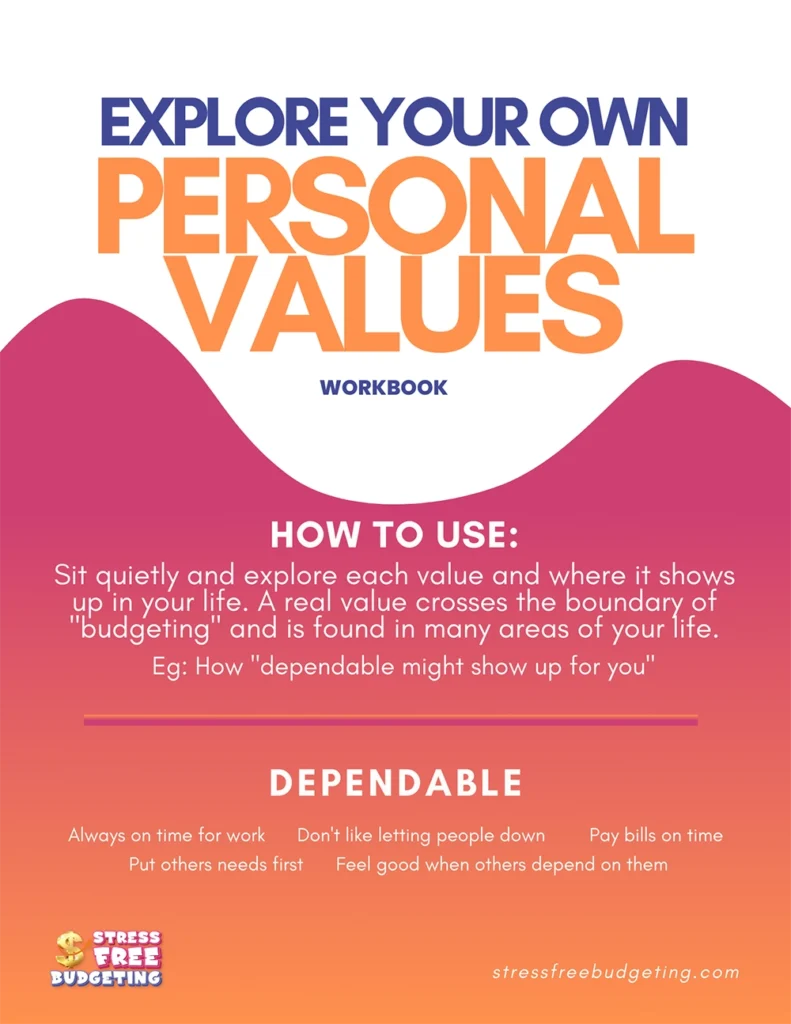

Confirmation shortcut means we often look for, understand, and remember things that agree with what we already believe. We then turn a blind eye to anything that doesn't fit with our ideas.

Picture this: Imagine a family that has a long-standing belief that traditional savings accounts are the safest and most secure way to grow their wealth, and they have always relied on these accounts to meet their needs.

But when they hear about alternative opportunities– like better money management strategies– they tend to ignore or dismiss these fantastic opportunities in favour of their deep-seated beliefs in the safety of savings accounts.

What makes this so deadly is that people inflicted with this shortcut are completely oblivious to their missed growth potential, and their finances stagnate.

Plus, when money is held in a savings account with interest rates lower than the inflation rate, its purchasing power diminishes over time.

If you would love to get an in-depth solution to this brain shortcut, I invite you to download the Explore Your Personal Values Workbook from our Affordable Money Wellness Collection.

This brain shortcut is a term used to describe how a person’s past experiences or memories (particularly childhood) can influence their perceptions, attitudes, or decisions in the present.

Now, I would like to ask you a question…

As an adult, do you get an anxious feeling whenever your partner picks up the healthier, but more expensive options in the grocery store? I hope not.

But if you do, is it because every little trip to the grocery store might get your mother worked up, and now you picked up on that habit? Or is it because you had a rough childhood, where splurging a bit on anything can make you feel insecure?

Your parents might have had a huge hand in that,

You see, parents are primary financial role models for their children. If your parents demonstrate responsible financial behaviours and instil good money habits in their children, such as budgeting, saving, and investing, you and your siblings are more likely to adopt these behaviours.

But if they show recklessness with their money, then there’s a good chance that you have mimicked their behaviours.

Additionally, other influential figures can also play a huge part in your childhood. Grandparents, guardians, or mentors can also shape your mindset and behaviours early in life. These individuals may give you sound advice or reinforce certain biases.

Traumatic experiences suffered in childhood can also influence this shortcut.

While physical scars stop hurting after a while, the psychological scars trauma leave us last for a lifetime.

This can be true during childhood when a family's bankruptcy, foreclosure, or extreme poverty can create traumas that reinforce fear, anxiety, and these brain shortcuts– making them overly cautious of every financial decision they make as adults.

No matter your background, it’s not mine to probe. However, by identifying and understanding this deep-rooted problem yourself, we can begin to change and progress your mindset– for the better.

First, we have to pause and reflect on the situation. Taking a moment to step back and giving yourself some time to let your emotions calm down before these impulsive decisions come into play is your best bet.

But if it’s too late to practice mindfulness and you’ve already let your emotions get the better of you, don’t beat yourself up! We all make these blunders from time to time.

However, instead of dwelling on them and negatively affecting your mindset, you can view them as “lesson learned” situations to improve your money habits.

You can also try to actively question your emotions and brain shortcuts.

When you catch yourself impulsively eyeing a flash sale, you can try to practice mindfulness and challenge your thoughts.

Alternatively having someone you can contact who can help you to step out of the emotions … offer coaching…

If you fail to do so, remember, it’s better to try than never at all!

Next, you need to find a sounding board you can bounce ideas off – like consulting your partner or hiring a professional.

I recommend discussing money management and huge decisions with them over a cup of coffee in the morning since they can offer you valuable support and be there for you when you need some guidance.

But if you would love some unfiltered advice (since family can often give you biased insights, and avoid starting a potential argument), I also recommend hiring a dedicated financial wellness advisor.

Not only are they great at helping you avoid emotions taking over your money management decisions, but they also offer you 1:1 coaching sessions to help you get the right mindset.

By doing these two things together when you’re faced with impulsive decisions, you’ll eventually notice that you’re on the right track to better money management.

But if you would love to access more resources…

…to help you deal with these emotions through proven and practical strategies, we invite you to grab our free Explore Your Personal Values Workbook from our Affordable Money Wellness Collection.

What’s this?

It’s a six-page workbook designed to help you discover what really matters to you taps into your emotions, and leaves you with a fresh, improved connection to money.

Money has the potential to evoke strong negative emotions within romantic and familial relationships, especially when you are tackling issues of control, trauma, power dynamics, feelings of inadequacy, and low self-esteem.

Your emotions can be tied to a lot of factors. Internally, your upbringing and surroundings play significant roles. Externally, peer pressure and the media you engage you consume are some of the major contributors.

Various factors heavily influence your outlook on money. Examples of these are family dynamics, health, career decisions, and age.

Your family and health can affect your life goals and how comfortable you are with taking risks, while your career choice can impact how much money you make and how much wealth or assets you accumulate.

Every day, we make loads of small decisions, many of which are secretly influenced by the way our minds think about money. These decisions can put up roadblocks in our mindset if we're not careful.

That's why it's super important to spot these habits and try to fix them ASAP – even if you're moving at a snail's pace.

Do you have any queries or thoughts to share? Feel free to reach out. If you found this guide particularly helpful, check out a few more helpful guides in my blog– I’m always here to support you in this journey towards better money habits!